One of the most infamous criticisms of China over the past several years that has formed the basis for viewing the country as an Orwellian surveillance state and its citizens as mere drone-like-automatons is its supposed “social credit system.” But what if I were to tell you that the origin of this Orwellian “social credit system” and the fintech (financial technology) credit loan bubble crises were actually created by the same Anglo-American institutions that also created the United States’ 2008 financial crisis? Or that fintechs such as Alipay, Antpay (both created by Jack Ma) and Wepay (Tencent) are not truly Chinese creations but have in fact been managed and funded by Anglo-American institutions that overlap heavily with Project Stargate? Or that China in fact cracked down on this back in 2020 which was portrayed by western press as a global scandal when the poor Big Tech billionaire Jack Ma was taken down a few pegs?

As this four-part series will go through in great detail, the reality was that these Big Fintech companies were giving out predatory loans on the level of what sparked the 2008 financial crisis. These Big Tech companies, like Alibaba and Tencent didn’t hold skin in the game and were going to come out on top, even if mass defaults of loan payments were to occur and which were already happening. This is something that even by a western viewpoint, should not be left unchecked. Alibaba and Tencent were effectively acting as banks while holding no responsibility of a bank. It was a powder keg ready to explode, and as I will showcase in this series, was engineered to do so.

In addition to this, these Big Tech giants Alibaba and Tencent, had created their own social credit scoring and were creating rewards and punishments based off of a user’s score that would determine what discounts/deals they would receive as a consumer on their platforms (think of Amazon, Apple Pay and Google Pay on steroids), or whether the penalised user would have limited access or temporary banning etc. to these platforms, such as music or films, video games, online shopping, restaurants, loans, rental deals on apartment units etc., thus, penalties meant you didn’t have full access or the best “deals” offered on their platforms.

Basically, think of a “Ready Player One” sort of world as the ideal for Big Tech. If you can get consumers to increasingly live their “reality” in a digital world, then who controls that digital world is like a God are they not? Well, you could say in 2020, Jack Ma was on a god-like high.

Alibaba and Tencent are still global giants in Fintech, however, they are beholden to proper banking regulation now which put at an end to the predatory loaning (they no longer give out P2P loans), as well as their reward and punishment social credit system. Thus, China clamped down on Big Tech’s social credit system and deemed it illegal to create rewards and punishments.

In truth, there is a double standard that is repeatedly applied to China. In this case, criticizing China for having been too lax on these Big Tech giants, which led to the P2P (peer-to-peer fintech loans) crisis that hit a boiling point in China from 2013-2018, and then when China regulates these Big Tech giants’ actions such that predatory actions are not tolerated, the West howls that China is being authoritarian. As we will see in this series, China’s P2P crisis was an Anglo-American construct, the same construct that also triggered the 2008 financial crisis within the United States.

In this series we will go through the history of how China clamped down on Big Tech in great detail, including members of its own government that were found guilty of corruption and went to jail. Yes, you heard right, China, unlike in the United States, responded to this financial crisis sparked by predatory loans by actually sending high-ranking government officials to jail.

Meanwhile, these very institutions continue to go largely unchecked in the West with the most recent BigTech Private Credit Loan bubble ready to burst in the United States. Even the former Goldman Sachs CEO who led the bank through the 2008 financial crash, Lloyd Blankfein, told the Telegraph recently that he “smells [another] crash coming.” The question is – is this just all reckless happenstance, or is it an engineered “reboot” of the financial system where Big Tech comes out on top?

As we will see, Goldman Sachs will play a central role in this story…

One example of Big Tech attempting to enter the banking world is Libra,[1] later called Diem, a stablecoin payment system proposed by U.S. social media company Facebook, that was ultimately rejected by U.S. regulators. The plan included a private currency implemented as a cryptocurrency. The launch was originally planned to be in 2020, the same year that China shutdown Jack Ma’s Ant IPO, what was to be the largest IPO in history.

Facebook’s bold attempt to create its own digital currency, if approved, would have had as its ultimate goal the eventual right to establish its own bank for said digital currency. It would not be long before other Big Techs would follow suit, such as Apple, Google, Amazon, Twitter X, Uber, DoorDash etc. With such a development, Big Tech would be in the position to give away risky loans, equivalent to loan sharking, with penalties if the borrower was late or defaulted on a payment.

In other words, these platforms could penalise a borrower by limiting or blocking their services to said borrower on platforms such as Facebook, Apple, Google, Amazon, Twitter X, Uber, DoorDash etc. etc. The reader should be aware that Apple Pay and Google Pay are already highly integrated into much of American consumer society.

Presently these companies do not have the right to give out loans or own their own bank, however, as we will see in this paper, fintech in the United States and Europe does have this right to give out P2P loans and own their own banks. It is only the merger of these consumer-based platforms mentioned above that are kept separate, however, massive pressure is whittling away at this flimsy barrier that is ready to break at any moment. In fact, Goldman Sachs is leading this charge into a “Ready Player One World” as we will soon see.

This had been something that was allowed to fester in China through Big Tech private credit loans such as Jack Ma’s Alipay and Antpay, along with WeChat pay (Tencent), something that had run amok earlier during their P2P crisis before the Chinese government began to clamp down, which led ultimately to the global scandal in 2020 when Jack Ma was taken down several pegs. The significance of this should be especially viewed in context to the fact that Alipay, Antpay, and Wepay are not truly Chinese companies but are funded and managed by powerful Anglo-American institutions as this paper will lay out.

This four-part series will showcase how not only are the origins of the social credit system not to be found in China, but that China had in fact blocked the attempt from Big Tech to essentially attempt a coup d’etat on its national banking/financial system. This series will go into great detail as to how this came about, as well as where the true origins of the social credit system lie. In Part III, we will discuss accusations of China using an Orwellian social credit system within their legal system, which we will see consists of a lot of hot air. Finally, in Part IV we will discuss what is China’s digital currency and how it differs from what Big Tech is attempting to bring about.

The 2008 U.S. Financial Crisis as a model for China’s P2P (Peer-to-Peer) Loan Crisis

In order to understand what hit China between 2013-2018 in their P2P crisis, we must first understand what the 2008 financial crisis was that hit the United States banking and financial system with catastrophic global effects – for it was this crisis that was the model used against China’s own banking and financial system.

Two especially big players that would play a prominent role in the U.S.’s 2008 financial crisis, were Prosper (f. 2005) and LendingClub (f. 2006), which were both founded in San Francisco, California.

Prosper is one of the first peer-to-peer lending platforms. Prosper specialises in personal loans, home equity loans, home equity lines of credit and open credit cards[2]. LendingClub is the first peer-to-peer lender to register its offerings as securities with the Securities and Exchange Commission (SEC) and to offer loan trading on a secondary market. At its height, LendingClub was the world’s largest peer-to-peer lending platform.[3] Both Prosper and LendingClub connect borrowers with investors directly with loan amounts ranging from $1,000 to $50,000. Since its launch, Prosper has facilitated over $28 billion in loans.[4]

However, Prosper and LendingClub, though the first P2P lenders in the United States were not the origin of P2P loans. That title belongs to Zopa Bank Ltd. which was founded in the United Kingdom in March 2005. Zopa Bank Ltd. is a British online bank which offers deposit accounts, personal loans and credit cards and is the world’s first P2P lending company, gaining a full banking licence in that eventful year of 2020 (the same year that Facebook’s Libra (Diem) attempted to get U.S. approval of its own digital currency and Jack Ma attempt to get approval for his Ant IPO in China).

The P2P side of Zopa closed in December 2021. It should be emphasized here that San Francisco-based Prosper was created on the very heels of Zopa, which is likely not a coincidence. Neobanks such as Zopa Bank, are fintech companies offering banking-like services and are growing in presence within western countries.[5]

Zopa, in turn, was created by the internet banking company Egg Banking. Egg, also headquartered in the United Kingdom, was founded in 1998. Egg was born out of the banking arm of Prudential, a British multinational insurance and asset management company headquartered in London and Hong Kong.

The reader should be reminded here that Hong Kong was a British colony for 99 years, part of the British Empire’s spoils from the Opium Wars and was only released back to China in 1997. However, there is still a great deal of pressure on China to stay out of the Hong Kong arena, with the “One Country, Two Systems” slogan (something that was promoted by the very British colonialists themselves) used to somehow justify keeping Hong Kong and Macau out of the Chinese government jurisdiction even though they are officially recognised as part of China.

To give the reader a quick and effective example of how much influence Britain continues to hold over Hong Kong banking, we only need to look at who actually controls its money supply. Hong Kong has a currency that is separate from the Chinese Yuan ¥, called the Hong Kong dollar $. The date of its introduction was 1846. The First Opium War was from 1839 to 1842. One of the consequences of China losing this war against Britain was the signing of the Treaty of Nanking, which gave British subjects extraterritorial privileges in treaty ports, especially in the region of Hong Kong. This forceful “opening” up of China to European trade was mainly in opium. And it is clear that the Hong Kong dollar was born out of this nefarious history.

Today, three banks control the printing of Hong Kong money: HSBC, Standard Chartered and the Bank of China. Only the Bank of China is an actual Chinese bank. HSBC and Standard Chartered are British banks with their headquarters in the City of London.

Thus, HSBC (a bank that has continued to be caught in dope and money laundering) has reserved the right to this day, the authority to print 1/3 of Hong Kong currency, the only other two allowed agencies being Standard Chartered Bank (another British multinational bank with headquarters in the City of London) and Bank of China, the only Chinese owned bank. In other words, China has the authority to only print 1/3 of Hong Kong currency even though Hong Kong is legally recognised as part of China. And this despite HSBC being on a blacklist of foreign companies in China.

Standard Chartered, along with HSBC, are both British dope banks that were founded in service to Britain’s opium trade. Standard Chartered was founded in 1853 and opened its first branches in Bombay and Calcutta (India), as well as Shanghai and Hong Kong (China). Britain had colonised India and was where the opium production was centered with China chosen to be its main consumer in the name of British “free trade.” HSBC was founded in 1865, as the name implies in both Shanghai and Hong Kong (for more on this story refer here).

It is these two old British banks that were created specifically for opium trading that control the majority of Hong Kong’s money supply to this day.

China has until recently, not been strong enough to take on these old British banks, however, the tides are changing.

Suffice to say, old British banks like HSBC, Standard Chartered and Prudential’s heydays in Hong Kong appear to be numbered.

Now back to our story.

With this added context in mind, it has been demonstrated that Zopa was born out of Egg Bank, which was in turn, born out of Prudential, a British multinational insurance and asset manager. Prudential was also founded during the Opium War era, in London in May 1848, with a focus on having a strong presence in Hong Kong.[6]

Prudential would become a market leader in asset acquisitions in the UK, notably in real estate. In 1986 they acquired the American insurer Jackson National Life for $608 million and by 2020 held $297.6 billion in total assets while still owned by Prudential. Jackson National Life Insurance Company is a U.S. company whose subsidiaries specialize in asset management and retail brokerage.

Prudential had also acquired that same year, in 1986, Reeds Rain, the second largest estate agent chain in the United Kingdom.

In 1998 Prudential set up Egg which created the first ever P2P loan lender, Zopa. Egg was later sold to Citibank in 2007. In December 2008 the Financial Services Authority fined Egg £721,000 for the persistent mis-selling of payment protection insurance (PPI) on its credit cards.[7] In 2011 Barclays Bank purchased Egg’s more than one million credit card accounts from Citigroup.

In 2004 Prudential launched a new subsidiary PruHealth, a joint venture with Discovery Holdings of South Africa selling private medical insurance to the UK market.[8]

In 2019 Prudential attempted to purchase the pan-Asian life insurance company AIG, American International Assurance (AIA) but the deal later collapsed.

In 2021, Prudential announced it was to focus solely on African and Asian markets.

Looking at this history one cannot help but be reminded of Blackstone, but with Prudential focusing on African and Asian markets while Blackstone focuses on American and European markets. Blackstone, founded in New York City in 1985, is the largest commercial landlord in the world and is what BlackRock was born out of.

Blackstone made a killing off of the housing bubble bust during the 2008 financial crisis and is a big reason why Americans can no longer afford to purchase a house of their own today.

Blackstone has had a long legacy of buying up American assets such as houses, hospitals, nursing homes, and schools. When these infrastructures such as hospitals and schools came under the ownership of Blackstone all sorts of budget cuts were made to the detriment of health and educational services, including food rations to patients. Blackstone had also acquired the largest physician staffing firm in the United States in 2017 resulting in low-income patients facing far more aggressive debt collection lawsuits.

In addition, Blackstone is responsible for buying up homes and is largely responsible for the inflation of house prices such that most Americans today cannot afford decent housing, in addition to hiking rent rates (for more on Blackstone refer here).

And not coincidentally, Blackstone is at the center of the U.S.’s private credit loan bubble crisis that is threatening a repeat of the 2008 financial crash.

Meanwhile, Blackstone’s spawn, BlackRock is still attempting to acquire 43 of the 53 CK Hutchison ports with China so far blocking the deal from going through, though the two ports in Panama have now been seized.

BlackRock just so happens to be the world’s largest asset manager, managing over $11 trillion of largely billionaire money. BlackRock was also officially brought in by the G7 to oversee acquiring infrastructure worldwide in service to the Partnership for Global Infrastructure and Investment (PGII), which was created to directly oppose China’s Belt and Road Initiative. BlackRock is working in partnership with Microsoft among other tech companies to accomplish this noble task. (For those who would like to know more about China’s BRI and its activities in other countries refer here)

Zopa was the first P2P loan lender, born out of the bowels of Prudential, however, fintech showed its real potential with the launch of the giants Prosper and LendingClub in the United States in 2005 and 2006 respectively.

Prosper is America’s first P2P lending marketplace with over $28 billion in funded loans.[9] Investors can consider borrowers credit scores, ratings, and histories and the category of loan. Prosper also offers tools for financial planning and credit monitoring.

Effective December 19, 2010, Prosper filed a new prospectus with the SEC, changing its business model to use pre-set rates determined solely by Prosper based on a formula evaluating each prospective borrower’s credit risk.[10] In other words, Prosper’s right to generate their own social credit system. Under the new approach, lenders no longer determine the loan rate via price discovery in an auction. Instead, they simply choose whether or not to invest at the rate which Prosper’s loan pricing algorithm assigns to the loan after it analyzes the borrower’s credit report and financial information.

Thus, Prosper decides the rate a borrower will be charged for borrowing depending on the credit score Prosper has created for them. The investor can either choose to accept this rate of charge for the loan or reject it, they are not able to change the determined rate decided by Prosper.

In fact, co-founder of Prosper Chris Larsen is known as a “Credit Score Pioneer.” Before founding Prosper, he founded E-LOAN in the early 1990s where he began his expertise in consumer credit scoring. He has also served on the board of Credit Karma, a credit and financial management platform that earns its revenue from lenders who pay the company when they successfully recommend a borrower to them.

It should also be noted that Chris Larsen went to Stanford University a Project Stargate recruitment hub.

In 2016, Prosper Marketplace unveiled Prosper Daily, a mobile app. The app is designed to give consumers tools to make financial decisions, including viewing all their financial accounts in one place, budgeting and tracking spending by category, identifying questionable charges, and monitoring their free credit score, which is updated monthly.[11]

Wikipedia writes:[12]

Prosper opened to the public on February 5, 2006, and was founded by Chris Larsen (the founder of E-loan) and John Witchel. Prosper is backed by BlackRock, Sequoia Capital, Accel Partners, Agilus Ventures, Benchmark Capital, CrossLink Capital, DAG Ventures, Draper Fisher Jurvetson, Fidelity Ventures, Omidyar Network (an investment vehicle of eBay founder Pierre Omidyar), Meritech Capital Partners, TomorrowVentures (an investment vehicle of Google Executive Chairman Eric Schmidt), and QED Investors (an investment vehicle of Capital One co-founder Nigel Morris).

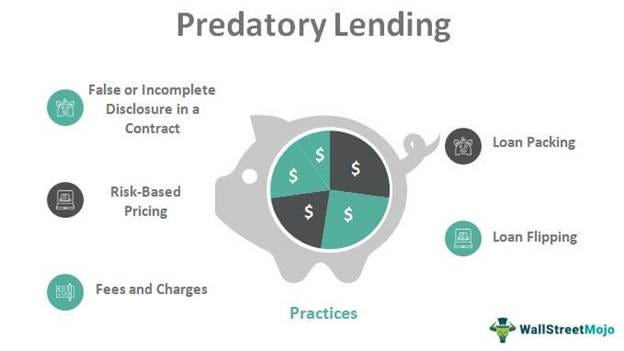

In 2008, the same year Egg was found guilty of persistent mis-selling of payment protection insurance (PPI) on its credit cards, the U.S. Securities and Exchange Commission (SEC) found Prosper to be in violation of the Securities Act of 1933, that was put in place as a response to the stock market crash of 1929. The 1933 Act is based upon a philosophy of disclosure, meaning that the goal of the law is to require issuers to fully disclose all material information that a reasonable shareholder would need in order to make up his or her mind about the potential investment. If the issuer fails to do this, it is considered a “predatory” loan.

‘As a result of the SEC’s findings they imposed a cease and desist order on Prosper. In July 2009, Prosper reopened their website for lending (”investing”) and borrowing after having obtained SEC registration for its loans (”notes”).[13] After the relaunch, bidding on loans was restricted to residents of 28 U.S. states and the District of Columbia. Borrowers may reside in any of 47 states, with residents of three states (Iowa, Maine, and North Dakota) not permitted to borrow through Prosper.’[14]

‘On November 26, 2008, a class action lawsuit was filed against Prosper in the Superior Court of California, County of San Francisco, California. The suit was brought on behalf of all loan note purchasers in Prosper’s online lending platform from January 1, 2006, through October 14, 2008, and alleges that Prosper offered and sold unqualified and unregistered securities in violation of the California and federal securities laws. The lawsuit sought class certification, damages, the right of rescission and the award of attorneys’ fees.’[15]

The lawsuit was settled July 19, 2013, for 10 million dollars paid in installments over three years.[16]

P2P lending platforms are selling themselves as the solution to the increasing impoverishment of the have-nots, when they are in fact the culprits behind predatory loans. And in the midst of the present BigTech Private Credit Loan bubble that threatens another financial crash on an even larger scale than what occurred in 2008, who do you think is going to foot the bill? The American people yet again of course, like they did back in 2008, only to go further and further into debt. This mounting debt will soon encompass social credit scores that will be created, managed and controlled by such benevolent fintech companies like Prosper and LendingClub, who in the latter case has even managed to purchase a regulated bank to service its financial schemes.

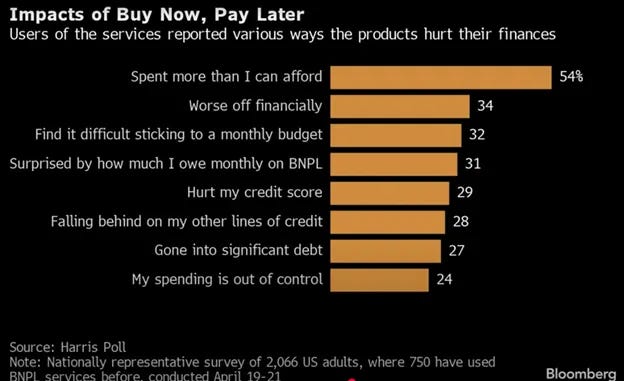

We are even seeing companies like DoorDash engaging in predatory lending with their “Buy Now, Pay Later” partnership with Klarna. Klarna is another fintech company and digital bank founded in Sweden in 2005 but headquartered in London.

Here’s what US consumers had to say in a poll about the “Buy Now, Pay Later” experience.

As for Prosper, in 2022, Forbes gave a negative review of the Prosper credit card. According to Forbes, “Prospering with the Prosper® Card* seems unlikely… We hope you live long and… well, apply for a different credit card.”[17]

And then there is this…

Wikipedia writes:[18]

In December 2015, the FBI reported that Syed Rizwan Farook, one of the shooters in the 2015 San Bernardino attack, had borrowed $28,500 from Prosper to finance the purchase of weapons and explosives. This was investigated by the FBI, the House Financial Services Committee, and the California Department of Business Oversight. The investigation was concluded with no action taken.

As already mentioned, LendingClub was the first American P2P to be registered with the SEC and at its height was the world’s largest P2P lending platform. In 2014, LendingClub raised $1 billion in what became the largest technology IPO of 2014 in the United States.[19] However, by 2020 LendingClub shut down its P2P lending platform after a series of scandals in 2016 made it difficult to attract investors.

Interestingly, LendingClub was initially launched on Facebook as one of Facebook’s first applications.[20] [21] After receiving $10.26 million in a Series A funding round in August 2007, from venture capital investors Norwest Venture Partners (which merged with Wells Fargo in 1998) and Canaan Partners, LendingClub was developed into a full-scale peer-to-peer lending company.[22]

Throughout the years it continued to raise funds from venture capital investors such as Morgenthaler Ventures, Foundation Capital, Union Square Ventures and Thomvest, owned by the family of Thomson-Reuters, owner of the Reuters news agency.[23] Thomson-Reuters founder Peter J. Thomson also invested an unspecified amount of his personal fortune into LendingClub.[24]

In 2012 LendingClub secured funding from another venture capital investor Kleiner Perkins Caufield & Byers and $2.5 million of personal investments from John J. Mack, former CEO and chairman of the board at Morgan Stanley (a powerful investment bank and brokerage firm). Kleiner Perkins partner Mary Meeker joined Mack on LendingClub’s board of directors.[25] In May 2013, Google Capital purchased a stake in LendingClub.[26]

In April 2015, LendingClub CEO Renaud Laplanche told Forbes that LendingClub would expand into car loans and mortgages.[27] LendingClub also announced a partnership with Google to extend credit to smaller companies that use Google’s business services.[28]

The company signed partnerships with Google, Alibaba, BancAlliance, and HomeAdvisor, including vetting community bank lenders for BancAlliance (a group of 200 banks), in order to send people on its platform to various community finance institutions.[29]

That same year, 2015, LendingClub partnered with Opportunity Fund, announced by former President Bill Clinton at the Clinton Global Initiative. The partnership intended to provide $10 million to small businesses in areas of California that are “underserved by lenders.” [30] [31]

LendingClub actually partnered with Prosper to provide personal loans in 2015 using small banks including Radius Bank, which was eventually purchased by LendingClub.[32] [33] American Banker news wrote back in September 2015, “For months, Prosper Marketplace and LendingClub have been teaming up with small banks that refer customers to their online lending platforms.”[34] In other words, for those turned away by small banks deemed “too risky” to qualify for a loan, such individuals or businesses were likely to be accepted for a loan by Prosper or LendingClub. This is exactly the sort of predatory loans that are fueling the Private Credit Loan crisis as we speak.

In 2016 LendingClub announced that its CEO Renaud Laplanche had resigned after an internal investigation found improprieties in its lending process, including the altering of millions of dollars’ worth of loans.[35]

Due to difficulties finding investors after the 2016 scandal, LendingClub had to eventually shutdown its P2P lending platform in 2020. That year, LendingClub announced that it would buy Radius Bank for $185 million in cash and stock.[36] The deal was the first time a U.S. fintech lender bought a regulated bank, positioning it one step further in becoming a marketplace bank.[37] In 2021, Radius Bank was integrated into the LendingClub brand.[38]

Radius had been founded in 1987 as First Trade Union Bank by the carpenters union in Massachusetts, using pension funds.[39] The bank, however, struggled during the subprime mortgage crisis (i.e. the 2008 financial crisis), when it invested heavily in commercial real estate. In 2014, it was renamed Radius Bank.[40] In June 2016, private investors had acquired approximately 95% of Radius Bancorp in response to Dodd Frank regulations.[41]

Here we see a very clear example of the sort of carnage that was a predictable outcome of the 2008 financial crisis, the end of small banks or in this case the actual acquisition of a small bank from a P2P fintech company, which has received almost all of its funding from venture capitalists, members of big banks and lots of old money.

LendingClub also operates an online-focused community bank headquartered in Lehi, Utah.[42]

In April 2026, LendingClub announced their pending rebrand to Happen Bank, a formal name change that will become active in July 2026.[43] Clearly LendingClub agreed they were in need of a facelift after years of scandal.

With this backdrop on the Anglo-American origins of P2P lending and fintech we are now ready to delve into China’s P2P crisis and how fintech giants Alibaba/Ant Group and Tencent/WePay that are commonly thought of as “Chinese” fintech fit into this Anglo-American picture.

The Origins of China’s P2P Crisis

China’s online peer-to-peer (P2P) lending industry launched in 2007, but the market didn’t experience its catastrophic crisis until a massive boom-and-bust cycle between 2013 and 2018. Over 6,000 platforms collapsed, wiping out billions in investments and sparking nationwide investor protests.

Thus, less than two years after the first P2P lending platform was created in the UK, quickly followed by the Americans, P2P lending platforms began a steady rise in China beginning in 2007, which promised to democratize finance and provide opportunities for young people. However, the ease of access to credit led to a cycle of serious levels of debt for many borrowers, resulting in a financial crisis. The crisis led to a crackdown on the P2P industry, with regulators tightening regulations and shutting down many P2P platforms. The details of how China cracked down on this will be discussed in Part II of this series.

The goal of P2P loan platforms is to offer borrowers loans that are provided by “peers” who accept repayment risk for a fee, hence the name peer-to-peer. While this sounds deceptively simple, the actual programs are complex. Several attributes that continue to make P2P lending attractive is that P2P loans don’t require an interview or going to the bank. You can apply online, and in general, the terms are more flexible. In many cases the borrower can go from application to receipt of funds within several days.

By digitizing everything and eliminating physical locations and highly paid employees – you’ve got a stripped-down internet loan machine that works 24/7 to connect borrowers to lenders. What makes P2P even more compelling is that it readily takes on individuals with bad or no credit scores, those who are underserved by traditional banks.

Though, this may seem like a very small portion of a western population, in Asia and especially Africa there is massive percentage of the population that still does not own a bank account. In the case of China during the advent of P2P loans, not only was this the case for most of its rural population but even those that owned a bank account would have limited or no access to a bank. This is because the number of physical branches were not enough to service the population and on top of this, if you happened to have a bank branch relatively close to where you lived, the lines were notoriously long and it was a normal occurrence to wait in line for hours to settle relatively simple matters.

P2P lending platforms offered to “resolve” these kinks in the system.

Richard Turrin writes in Cashless: China’s Digital Currency Revolution:[44] (note: SEC is in reference to the Securities and Exchange Commission within the United States)

The P2P concept is straightforward but the history of P2P in the U.S. should have been fair warning to China that this market was best not left to its own devices. Starting in 2006, P2P lenders in the U.S. operated without much regulation. The early versions of these companies had few restrictions on borrower eligibility. This caused adverse selection, attracting borrowers who would default on their loans, resulting in high loss rates. Still according to the U.S. Federal Deposit Insurance Corporation (FDIC), by the end of 2007 the P2P market had an estimated volume of $600 million. Perhaps not enough to ruffle the incumbent banks, but certainly enough to draw the attention of the Securities and Exchange Commission (SEC).

By early 2008, the SEC closed shop on all P2P lenders, including Prosper. In what would later turn out to be a stroke of genius [or insider information], Lending Club voluntarily ceased operations in 2007 just before the SEC closure. The SEC closed these lenders because it deemed that the notes issued to the lenders could be considered securities offered to the general public, and as such, amounted to investments. Consequently, P2P lenders would have to be registered by the SEC and cease operations until they received the necessary certification. In another interesting twist, the SEC commented that there was “no alternative regulatory scheme” that could adequately reduce investor’s risk. The SEC essentially admitting that P2P had no regulatory home [within the United States], a problem that would also plague China’s P2P market.

One reason why the SEC came down so hard was the prior abuse of sub-prime lending that contributed to the [U.S.] financial crisis. Raising the stakes for [U.S.] P2P lenders by requiring them to acquire a costly SEC registration resulted in the closing of all but Lending Club and Prosper.

When Lending Club reopened in 2008, it was a different world, one that was desperate for credit…and they were now the only game in town. Prosper opened six months later but was never able to overcome the delay.

The reason this is so important is that it demonstrates the efforts the SEC made in 2007 to regulate the P2P market in the U.S. Interestingly, these steps were taken after the lending market was launched, reinforcing the point that the speed of new technology adoption may exceed regulators’ ability to react.

The factors that made P2P so popular in the U.S. helped propel it to even greater heights in China. The ease of using online platforms (in a country with a significant unbanked population) [author’s note: unbanked in reference to having no bank account] made it an immediate success. The ability of P2P to provide credit for the masses of SMEs [Small and Medium Enterprises] was both practical and essential in speeding China’s development, and senior officials publicly praised the new system. Sadly, much of this praise would later be manipulated by P2P lenders to entice investors.

As noted previously, a critical feature of P2P lending is its availability to those with low credit scores. This is perfect for China, where there were no credit scores for the majority of the population…the national credit scoring didn’t exist in China until the founding of government sponsored Baihang Credit arrived in 2018. The PBOC did have the Credit Reference Center founded in 2006, but it had access only to bank data on personal account balances.

The lack of credit rating technology contributed to making bank lending next to impossible for ordinary people, who had no data for the banks to evaluate. That P2P lending could circumvent the banks and deliver a loan to someone who had never borrowed before and had no history was, and remains, a significant accomplishment. To fill this gap, Ant Financial and Tencent [devoted] tremendous resources to developing credit scores based on big data on their internet platforms. In the absence of credit ratings, big data [appeared] a logical alternative…

The rise of P2P loans in China was further inflamed by the West’s own 2008 financial crisis which created a rapid drop in factory orders, which caused the government to rely on credit to compensate for the loss in funds.

We should really take a moment to pause here and let this sink in.

The timing of the creation of P2P loans could not have been better. As the 2008 financial crisis hit the world, not only within the United States, but businesses around the world were in desperate need for loans as profits began to tank globally.

Richard Turrin writes:[45]

Most of the P2P companies did away with the direct matching of borrowers to lenders, and instead used a portfolio of loans (fund pools) whose constituents were impossible to check.

Investors received returned based on the portfolio’s performance, essentially a black box, and as along as the returns kept flowing, no one ever asked what was inside. Perpetuating this particular fraud is even easier for the P2P company, as a company did not need to show actual borrowers’ personal IDs. Dangerously, it gave the P2P company total control of the value of the pool. There is a certain irony that the assembly of these [Chinese] loan portfolios closely resembled sub-prime loan securitization in U.S. markets, which had similarly disastrous results.

During the run-up to the disaster many P2P lenders moved out of matching personal loans and into business lending creating securitization-like structures reminiscent of notorious Collateralized Debt Obligations (CDOs) in the U.S. market. P2P lenders had gone full circle to become quasi-banks, and all of their activities were “guaranteed.”

The transactions grew so large that the entire P2P sector became known as the “shadow banking system,” given that they supported China’s corporate debt from companies large and small. P2P lenders would regularly make loans to sizable companies who had been rejected by banks or could not even apply. To be fair, the problem for small and medium enterprises (SME) businesses in China was not one of creditworthiness. Many SMEs were simply not well served by banks and had no other route apart from P2P lenders or local loan sharks.

…

As if the news of P2P failures wasn’t disruptive enough, it was followed by the 2015 summer Shanghai Stock Exchange “turbulence” that removed about one-third of the market value. This shocked the system, laying bare P2P’s excesses and removing any hope of piloting the P2P market to a soft landing. Many of the P2P loans had gone to finance purchases of equities and housing down payments that helped fuel bubbles in both markets.

The market turmoil forced massive regulatory changes, in an interesting parallel with U.S. regulators and the sub-prime crisis. Regulators made the crucial decision to put P2P lenders under the China Banking Regulatory Commission. China’s regulators also began an extensive campaign to warn investors about the perils of P2P loans. These warnings fell on deaf ears due to China’s extraordinal high growth, nearing eight precent in prior years. People were still investing.

P2P platforms with the new law were prohibited from financing their own projects, depriving them of the ability to build Ponzi schemes. Rules also put caps on loans.

These laws fundamentally deleveraged the P2P business model and were prudent. They forced P2P lenders back into their traditional role of intermediaries rather than acting as shadow banks. Many P2P lenders found it impossible to support their existing business with such a highly constrained portfolio.

China’s P2P lending started in 2007. Recall the first P2P lenders were Zopa in the United Kingdom in 2005, followed by Prosper in 2005 and LendingClub in 2006 both established in San Francisco, California. It was these three, which formed the complex algorithm that was then used around the world, in spreading the epidemic of predatory P2P loans.

The largest predatory P2P lender in China was eZuBao, established in Feb. 2014, a subsidiary of Yucheng Group. eZuBao’s total transaction volume had amounted to 74.568 billion yuan (which is $10.998 billion USD) with 909,500 investors deceived.[46]

At the end of 2015, eZuBao was investigated for fraud by the Chinese authorities. Subsequently, relevant leaders of Yucheng Group and eZuBao were arrested by police on suspicion of fraud. On January 31, 2016, Xinhua News Agency revealed that eZuBao had illegally raised over 50 billion yuan ($7.375 billion USD), with victim investors spread across various regions of mainland China, totaling more than 900,000 persons.[47] eZuBao was shutdown Dec. 2015 by the Chinese authorities as a Ponzi scheme.

The former Chairman and founder of Yucheng Group, Ding Ning, who created and controlled eZuBao, was sentenced to life imprisonment in Sept. 2017 by the Beijing First Intermediate People’s Court for the crimes of fund-raising fraud, smuggling precious metals, illegal possession of firearms, and illegal border crossing.[48]

What is especially striking in this case, the largest P2P fraud case in China, is that Yucheng Group is registered in the British Virgin Islands, an Anglo-American tax haven. The relevance of this will become even more striking when we look into the cases of Alibaba and Tencent.

P2P lending in China is now completely gone, with the last P2P lender having closed in November 2020. However, P2P lending continues throughout Europe and the United States today.

Who Really Created Alibaba and Tencent Chinese Fintech Giants?

The most powerful P2P platforms in China were, however, from Alibaba and Tencent. Alibaba and its affiliate Ant Group, along with Tencent, still operate in China, however, they have been forced to shutdown their P2P lending platforms, the most lucrative aspect of their business due to China’s enforcement on regulation. With this forced “skin in the game” Alibaba and Tencent could not afford to continue operating as P2P lenders.

It should be noted here, P2P loans are not illegal, not in the United States nor China. P2P loans can operate legally and there were some in China that were legal or were operating within the realm of “moral hazard” which is a fancy word for saying that if something is immoral or unethical but legal there is nothing “technically” wrong with what you are doing. It became a ubiquitous term throughout the 2008 financial crisis.

Thus, P2P loans are technically legal, however, most were operating without skin in the game. It comes to a matter of how a country decides to regulate P2P lenders, which again is a relatively new phenomenon. With no real overhead cost and no real loss if a loan is defaulted on, many P2P lenders were found guilty of giving out predatory loans if not of even more serious crimes.

Recall, both Prosper and LendingClub were accused of predatory lending and settled out of court, both still operate in the U.S. today. As we will see in Part II of this series Goldman Sachs was also under investigation.

It was this new Chinese regulation at the 11th hour, enforced “skin in the game,” that costed Ant’s IPO in 2020, what was to be the world’s largest in history if it had been allowed to go through unchecked. The reader should be aware that this decision also costed China heavily in its growing stock market, and their financial markets were set back greatly due to this decision.

Effectively the Chinese government decided that they rather go through this fallback on their stock and financial markets which was quite significant, rather than run the risk of Ant not being “good for the money.” In other words, in 2020 Ant Group was claiming that their practices were legit and not a repeat of China’s P2P crisis (which unleashed carnage and mayhem between 2013 and 2018). However, because the amount in P2P loans from Ant Group were at the levels just before the P2P loan blowout just a few years prior and fast exceeding those levels, China decided it best to slam on the brakes.

And the new regulation did just that. P2P lending was no longer considered profitable in 2020, and the outcome was that there have been no P2P lenders since 2020 operating in China. Again, the details of this story will be discussed in Part II of this series.

In this paper we will focus on who created and funded the Fintech giants Alibaba and Tencent.

Let us start with the Alibaba Group.

Alibaba was founded in 1999. As the story goes, on June 28, Jack Ma with 17 friends and students founded Alibaba.com in his Hangzhou apartment. In less than four months, Alibaba received $25 million USD in investment from Investor AB,[49] Goldman Sachs and SoftBank.[50]

How did a practically non-existent tech startup from a man that was relatively unknown in the field manage to get such a tremendous sum from three of the most powerful banks in the world in a matter of a couple of months?

The answer to this question lies with Joseph Tsai, the true creator and manager of Alibaba who is the Chairman of Alibaba and has held the roles of chief operating officer, chief financial officer, executive vice chairman and founding board member of Alibaba. Tsai became Alibaba’s executive vice chairman in 2013 and became chairman of the company in 2023. He has become the second-largest individual shareholder of Alibaba after Jack Ma.

Joseph Tsai’s family lineage is an especially interesting one. His grandfather, Ruchin Tsar was part of the Kuomintang (KMT) and close to its leader Chiang Kai-shek. The KMT were forced to flee mainland China and installed themselves on the island of Taiwan after losing the Chinese civil war to Mao’s forces.

According to Tsai’s Baidu Wiki page, Ruchin Tsar served under the Shanghai gangster Du Yusheng, a Chinese mob boss who was close to Chiang Kai-shek. Du Yusheng made his fortune in the opium trade before transforming into a financial tycoon. Du Yusheng joined the notorious Green Gang at the age of 16, who were also affiliated with Chiang’s Kuomintang. It was said that Du Yusheng ‘surrounded himself with White Russian bodyguards.’[51]

Wikipedia writes:[52]

By the 1930s, Du controlled much of Shanghai’s gambling dens, prostitution, and protection rackets. With the tacit support of the police and colonial government, he also now ran the French Concession’s opium trade, and became heavily addicted to his own drug. Du had close ties with Chiang Kai-shek, who in turn had ties to both the Green Gang and other organised secret societies from his early years in Shanghai. In April 1927, Du, along with his sworn brothers Huang Jinrong and Zhang Xiaolin, conspired with Chiang to form the Chinese Progress Association (中华共进会), a para-militant group masquerading as a left-wing group to prepare for Chiang’s coup.

[When this coup failed] in 1949, on the eve of the fall of Shanghai, Du moved to British Hong Kong…

For those who are not already aware, it was through Chiang Kai-shek, who worked with Anglo-American players, that the opium trade boomed in China. Recall that Hong Kong, along with Shanghai, were part of the British spoils from the two Opium Wars. Hence the dope bank HSBC, a city of London bank officially named the Hong Kong Shanghai Banking Corporation. Chiang continued to work for Anglo-American institutions including the CIA in the opium trade with Taiwan and Hong Kong helping to facilitate the infamous Golden Triangle, with Chiang controlling Taiwan and Britain controlling Hong Kong. For more on this story refer here. And also here.

Ruchin Tsar was also an adviser to the Kuomintang government of nationalist leader Chiang Kai-shek[53] who established the Republic of China (ROC) in Taiwan (not to be confused with the People’s Republic of China (PRC) which is China’s mainland government). It was the ROC, under Chiang who ruled as a dictator of Taiwan, who worked closely with the CIA in opium production. This money was in turn used by both sides to fund paramilitary groupings. Again, for more on this refer to my paper here.

This lineage of Joseph Tsai is no small deal and gives us our first stepping stone in understanding where Tsai’s true allegiance lies. And as we will see, many of the Anglo-American institutional players in our story will have also played a role in opium to this very day.

Joseph Tsai’s wife, Clara Wu Tsai, is the granddaughter of Wu San-lien, the first elected mayor of Taipei City, Taiwan. Taipei is the capital of Taiwan. Thus, Wu San-lien was an important and close ally of Chiang, the latter who ruled over Taiwan from 1945 until his death in 1975, a thirty-year dictatorship (as in he was never elected and there were never any elections under his rule).

Thus, Clara Wu Tsai, like her husband, also comes from a prestigious political lineage of the Taiwanese aristocracy. Clara went to the elite Lawrenceville School, the same school as we will see that Joseph Tsai went to. She then went on to graduate from both Stanford and Yale.

Clara Wu Tsai serves on the board of trustees of Stanford University (a recruitment hub for Project Stargate).[54] The Standford University’s Neuroscience Institute is named after her, basically in return for the very generous funding by the Tsais’ for Stanford’s neuro research. In addition, Yale University has created the Wu Tsai Institute, which includes the Center for Neurodevelopment and Plasticity, the Center for Neurocognition and Behavior, and the Center for Neurocomputation and Machine Intelligence.[55] Clara is also on the REFORM Alliance board, which includes Jay-Z as a board member, that focuses on “prisoner rehabilitation.”

Joseph Tsai’s father, Tsai Chung-tsai, became the first student from Taiwan to earn a J.S.D. degree from Yale Law School in 1957. Chang Tsai & Partners is one of the top three private law firms in Taiwan founded by Joseph Tsai’s father and grandfather.[56]

Joseph Tsai was born in Taiwan. However, at a very young age moved to Canada. At the age of 13 he was sent to the Lawrenceville School in New Jersey, one of America’s most prestigious boarding schools. He then enrolled at Yale in 1982 earning a B.A. in Economics and East Asian studies.

In 1990 he earned a Juris Doctor (J.D.) from Yale Law School. That same year he was hired by the Wall Street law firm Sullivan and Cromwell, a law firm that has employed many a prominent CIA agent, including CIA godfather and Council on Foreign Relations president Allen Dulles. Foster Dulles also worked at Sullivan and Cromwell, who was the U.S. Secretary of State under Eisenhower and worked lock and step with CIA Director Allen Dulles.[57]

After three years at the law firm, Tsai switched to private equity and joined Rosecliff, Inc., a small management buyout firm based in New York, as vice president and general counsel. He left for Hong Kong in 1995 to join the Swedish Wallenberg family’s investment conglomerate Investor AB, where he was responsible for its Asian private equity investments.

It just so happens that Joseph Tsai meets Jack Ma for the first time ever right around the time Ma comes up with the idea for Alibaba.com. As in a matter of a couple of weeks or less. Joseph Tsai is apparently so excited over this business venture that he not only quits his lucrative job with Investor AB and accepts a pittance first-year salary of $600 in total but is the guy who convinces three of the most powerful banks in the world to invest in Jack Ma’s “concept” at the drop of a pin.

As the story goes, in August 1999, less than two months after Ma comes up with the idea for Alibaba, Tsai persuades Goldman Sachs to invest in Alibaba.[58] In October of that year, Goldman Sachs led a consortium of institutions including Fidelity Capital, the Singapore Government Technology Development Fund, and Investor AB (Joseph Tsai’s former employer) to invest $5 million in Alibaba. In the same year, Joseph Tsai led the establishment of Alibaba Group’s Hong Kong headquarters.[59]

This all happened in less than four months from Ma’s brainstorming session in his apartment with no previous experience with anything on this level or scale.

In 2000, Tsai takes Ma to Japan to meet Masayoshi Son, the eccentric billionaire of SoftBank and persuades him to invest massively in Alibaba, $20 million USD to be exact.[60]

Before we go further, let us look into who the Wallenberg family is and SoftBank.

The Wallenberg family’s own stakes in Swedish companies is worth over $600 billion. This includes ABB (Swedish-Swiss technology company), Ericsson (Swedish multinational networking and telecommunications company), AstraZeneca (a Swedish-British multinational pharmaceutical and biotechnology company with its headquarters in Cambridge, UK), SEB Bank (translates to “Scandinavian Private Bank” headquartered in Sweden), SAAB (Swedish Aerospace and Defence) and 30 other corporations.

In the 1970s, the Wallenberg family businesses employed 40% of Sweden’s industrial workforce and represented 40% of the total worth of the Stockholm stock market.[61] Their flagship company, Investor AB, has a market capitalization of over $100 billion and is Sweden’s most valuable publicly traded company.[62] Because of their massive stake ownership in Swedish companies, 40% of the Swedish stock market moves based on the decisions made in the Wallenberg private offices.

This is who Joseph Tsai stopped working for to embark on this project with the unknown and relatively unaccomplished Jack Ma. However, when we see how readily these powerful banks poured millions into this project with Joseph Tsai at the helm, it looks like Tsai never really took a gamble on Ma, but was clearly given the blessing from these high-level players in finance to head the Alibaba project with full support from most notably the Wallenberg family (Investor AB), SoftBank and Goldman Sachs who would not have come to the table without Tsai.

SoftBank is a Japanese bank, a multinational investment holding company headquartered in Tokyo. Part of its focus in investment is AI, biotechnology and robotics. SoftBank has a history of working very closely with American Big Tech.

In order to see what SoftBank is a part of, besides what gave Alibaba its meal ticket, we will have to go through a bit of a rabbit hole so bear with me, but I promise you, all the names of the institutions that are being brought up are to paint a coherent picture at the end of this. This is especially important to understand since, as we will soon see, SoftBank is a co-founder and primary funder of Project Stargate.

In the 1990s SoftBank formed a joint venture with Yahoo! creating Yahoo! Japan (now LY Corporation).[63] In 2000, as already mentioned it invested heavily in Alibaba, a project that essentially had been given the blessing of the global power-house Goldman Sachs.

In May 2015, Masayoshi Son (founder of SoftBank) said he would appoint Nikesh Arora, a former Google executive, as Representative Director and President of SoftBank. Arora had been heading SoftBank’s investment arm.[64] In 2016, amidst pressure Arora steps down and is replaced by Baer Capital Partners (an apparently unregulated holding company) founder Alok Sama.[65] [66] Baer Capital Partners is headquartered in London, England and was founded in 2006 to provide growth capital and financial advisory services.

On 6, December 2016, after meeting with United States President-elect Donald Trump, Masayoshi Son announced SoftBank would be investing US$50 billion in the United States toward businesses creating 50,000 new jobs.[67]

On 14, November 2017, SoftBank agreed to invest $10 billion into Uber.[68] On 29 December 2017, it was reported that a SoftBank-led consortium had invested $9 billion into Uber. The deal, to close in January 2018, would leave SoftBank as Uber’s biggest shareholder, with a 15 percent stake.[69] The deal was secured after Uber shareholders voted to “sell their shares to the Japanese conglomerate at a discounted price.”

On 1, March 2018, SoftBank’s Vision Fund led a $535 million investment in DoorDash.[70] On 27 September 2018, SoftBank announced the investment of $400 Million in Home-Selling Startup Opendoor.[71]

Opendoor Technologies Inc. is an online company that buys and sells residential real estate. Headquartered in San Francisco, it makes instant cash offers on homes through an online process, makes repairs on the properties it purchases and re-lists them for sale. It also provides mobile application-based home buying services along with financing. As of November 2021, the company operates in 44 markets in the U.S. Basically buying and selling houses as an online company.

Property owners bid to sell their properties on the online platform. When a bid is accepted, Opendoor purchases the property as-is, charging a fee comparable to the commissions real estate agents collect in return for the convenience of closing a sale quickly without home showings.[72]

In August 2019, Opendoor launched mortgage services through Opendoor Home Loans.[73]

On December 21, 2020 Social Capital Hedosophia Holding Corp II[74] finalised its merger with Opendoor. Social Capital Hedosophia Holdings Corp. II is a Cayman Islands-based SPAC formed to pursue mergers or acquisitions in the technology sector.

On August 1, 2022, the Federal Trade Commission reported that Opendoor had agreed to pay a settlement of $62 million over charges of misleading potential home sellers in its marketing campaigns.[75] [76]

It should be noted that all of these online companies are headquartered in California, with many in Palo Alto and San Francisco as their hub. Again, this is very relevant to Project Stargate.

SoftBank continued to invest heavily in Alibaba including $10 billion stake under former president of SoftBank Alok Sama.[77] However, between 2020 and 2024 SoftBank dropped all of its investment into Alibaba despite its business continuing to boom.

That same year, the year that China clamped down on Alibaba, Ant and Tencent, and crushed Ant’s hope of achieving the largest IPO in history, Jack Ma was forced to step down from SoftBank’s board of directors on June 25, 2020.[78] This marked the end of his 13-year tenure as a SoftBank board director.

In other words, the year that China reigned in Alibaba/Ant Group and forces them to be beholden to Chinese regulation is the year SoftBank drops Jack Ma like a sack of potatoes.

It should also be noted here that SoftBank has created the SoftBank Vision Fund the world’s largest technology-focused investment fund, specializing in AI, robotics, and advanced technologies with over $166 billion in assets under management.

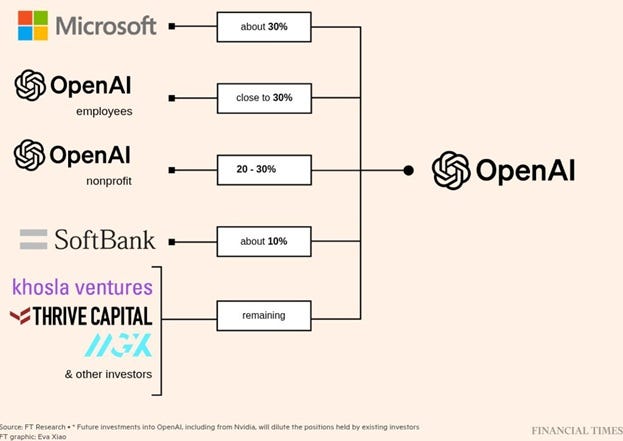

Though the founder of the SoftBank Vision Fund (2017) is Masayoshi Son who is Japan-based, the Fund is headquartered in London, England. Notable investments by Softbank Vision Fund include OpenAI, where SoftBank committed over $60 billion for ~13% ownership.[79]

In addition, SoftBank owns SB Cayman, an offshore investment holding company in the Cayman Islands which is primarily operating under the umbrella of SoftBank Vision Fund.[80]

In May 2024, SoftBank launched a joint venture with healthcare technology company Tempus AI. The aim of the venture was to provide precision medical services in Japan by utilising AI.[81]

In December 2024, it was reported by CNBC that Softbank plans to invest $100 billion in the US over the next 4 years, with funding coming from various sources controlled by Softbank, including the Vision Fund, capital projects or chipmaker Arm Holdings. The investment is said to create 100,000 jobs focused on artificial intelligence and related infrastructure.[82] [83]

In January 2025, SoftBank Group, Oracle Corporation, MGX [Saudi Arabia], OpenAI, and other partners established The Stargate Project as a cooperative venture aimed at building AI infrastructure in the U.S. With an estimated $500 billion in investment, the program seeks to generate 100,000 new jobs in the U.S. by 2029.[84]

In February 2025, SoftBank announced a joint venture with OpenAI called SB OpenAI Japan which would develop “Advanced Enterprise AI” called “Crystal Intelligence.” SoftBank would spend $3 billion annually to deploy OpenAI solutions across SoftBank companies. The 50:50 joint venture of OpenAI and SoftBank will “serve as a springboard for introducing AI agents tailored to the unique needs of Japanese enterprises.”[85]

On April 23, 2025, Cantor Equity Partners, a SPAC announced a merger with Twenty One (XXI), a bitcoin acquisition company. SoftBank will own a 25% stake in the business led by stablecoin issuer Tether and bitcoin exchange Bitfinex.[86]

In October 2025, SoftBank Group announced an agreement to acquire the ABB Robotics division from the Swiss industrial technology company ABB for an enterprise value of US$5.375 billion, replacing ABB’s earlier plan to spin off the unit.[87] [88] SoftBank chairman and CEO Masayoshi Son described the acquisition as part of the company’s strategy to expand into “Physical AI,” combining ABB’s robotics capabilities with SoftBank’s expertise in artificial intelligence and next-generation computing.

In October 2025, SoftBank Group approved a second installment of $22.5 billion to complete its $30 billion investment into OpenAI.[89]

On December 29th, 2025, SoftBank Group announced an agreement to acquire U.S.-based digital infrastructure investment firm DigitalBridge Group, Inc. in an all-cash transaction valued at approximately $4 billion. The deal, which would take DigitalBridge private, reflects SoftBank’s continued expansion into artificial intelligence–related infrastructure, including data centers, fiber networks, and wireless assets. DigitalBridge is expected to continue operating as an independent investment platform following the completion of the acquisition, which remains subject to regulatory approvals.[90]

In February 2026, SoftBank Group’s investment into OpenAI exceeds $30 billion USD, accumulating an 11% stake. SoftBank is also presently in talks to invest as much as $30 billion USD more in a round that would value the startup at about $750 billion to $830 billion USD.[91]

SoftBank Group announced plans to invest up to €75 billion to develop 5 gigawatts of AI data center capacity in France, stating that it would be its largest AI infrastructure investment in Europe. The project is expected to create thousands of jobs across data center development, engineering, energy systems, robotics, operations, maintenance, and advanced manufacturing.[92] [93]

SoftBank is the third largest stakeholder of OpenAI after OpenAI, and Microsoft.

SoftBank is a 40% owner of Project Stargate.

That was the largest rabbit hole I expect to take you in this paper, though I hope you found that rabbit trail useful in mapping out who is really behind the “Ready Player One” dream.

The third large donor to Alibaba in its embryo state back in 1999 was Goldman Sachs, arguably the largest investment bank in the world. We will discuss more on Goldman Sachs soon. However, for now I hope the colossal status of these three funders to a start-up which hadn’t even been fleshed out yet is beginning to sink in. As we have and will see, both SoftBank and Goldman Sachs in particular are deeply embedded and invested in Project Stargate.

Back to Joseph Tsai, the man who brought the Wallenberg family, SoftBank and Goldman Sachs to invest in Alibaba, or was he hired by them?

Soon after meeting Ma, Tsai quit Investor AB and joined Alibaba’s founding team. He eventually held the roles of chief operating officer, chief financial officer, executive vice chairman and founding board member of Alibaba. Drawing from his background in corporate law and finance, Tsai led efforts to establish Alibaba’s financial and legal structure.[94] Tsai was clearly running the entire ship.

He became Alibaba’s executive vice chairman in 2013 and became chairman of the company in 2023. He has become the second-largest individual shareholder of Alibaba after Ma.[95]

In 2004, together with his former colleague Alexander West from his old employer Investor AB (the Wallenbergs), he established a hedge fund called Blue Pool Capital in Hong Kong, China.[96]

In August 2005, Joseph Tsai led the negotiations for the acquisition of Yahoo China and Yahoo’s investment in Alibaba Group. After the deal was completed, Alibaba not only received $1 billion from Yahoo but also acquired Yahoo China’s assets worth $700 million. This transaction also provided Alibaba with ample resources, laying a solid foundation for the subsequent development of Taobao, a Chinese online shopping platform. Later, under Joseph Tsai’s leadership, Alibaba successively acquired several well-known internet companies including AutoNavi, YTO Express, Youku, and UCWeb.[97]

In 2013, he stepped down as Alibaba’s Chief Financial Officer and became the Executive Vice Chairman of the Group’s Board of Directors. In 2014, Joseph Tsai led the company’s IPO and established its strategic investment team.[98] As we will see, Alibaba’s IPO was run and managed by six behemoth western banks.

In July 2015, Jack Ma and Joseph Tsai, following the example of former Google CEO Eric Schmidt, established their own family office, managed jointly by Oliver Weisberg, Managing Director of the hedge fund Citadel in Hong Kong, and Blue Pool Capital.[99] Citadel is an American multinational hedge fund and financial services company, it has more than $67 billion in assets under management as of January 2026.[100]

By the end of 2017, Alibaba had conducted $80 billion in strategic investments, overseen by the Alibaba Strategic Investment Department led by Joseph Tsai.[101]

There is one other notable character that influences Alibaba and that is J. Michael Evans. Evans is a Canadian technology executive and the President of Alibaba Group. And he just so happens to have spent 20 years working for U.S. investment bank Goldman Sachs before becoming president of Alibaba, a position he continues to hold today.

Evans had worked as Vice Chairman of Goldman Sachs and Chairman of Goldman Sachs Asia and spent 19 years as a Partner after joining the firm in 1993.[102] So, Evans was a massive Goldman Sachs player before accepting the Presidency of the Alibaba Group.

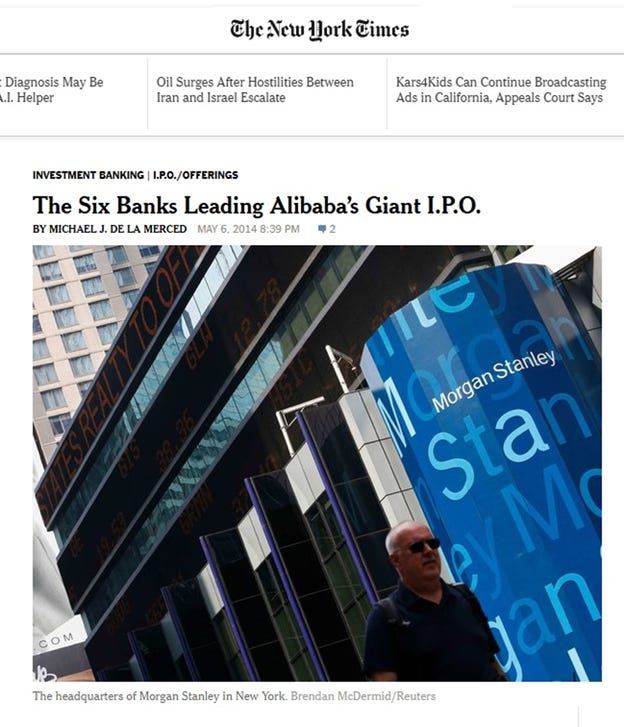

In fact, the six banks that led Alibaba’s Giant IPO, the second largest in history…

…were Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase and Citigroup.

The New York Times writes:[103]

Six firms were listed as Alibaba’s lead underwriters, listed mostly in alphabetical order: Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup. They emerged as winners for the honor of running an I.P.O. that could ultimately end up raising more than $20 billion…For months, Wall Street firms competed fiercely for the chance to take a piece of the stock sale.

…Top banks pulled out the stops, sending top deal makers to Asia to meet with top executives at the Chinese company, notably its founder, Jack Ma, and vice chairman, Joseph Tsai. JPMorgan Chase’s chief executive, Jamie Dimon, for instance, attended a dinner held for Mr. Ma in Hong Kong last year.

…The six banks listed on Alibaba’s prospectus officially are regarded as having equal status as lead underwriters, with a say on important I.P.O. matters, according to people with direct knowledge of the matter.

…Two of the firms undeniably had longstanding relationships with Alibaba. Credit Suisse and Morgan Stanley worked with the e-commerce concern well before it attained its sky-high valuations, including on fund-raising rounds in recent years.

Both firms were the main drafters of the prospectus…

…Two prominent banks are notably absent from the list. Bank of America Merrill Lynch and UBS did not receive spots in part because they are working on the forthcoming I.P.O. of JD.com, a competing Chinese Internet retailer backed by Alibaba arch-rival Tencent, according to people briefed on the matter.

So in reality, the giant Alibaba fintech company threatening China’s banking and financial system, was in fact led and funded by giant western banks!!! More on this in Part II of this series.

In 2019 Evans was charged for his involvement in the 1MDB scandal, which took place during his time at Goldman Sachs. The 1MDB scandal was a massive international financial fraud involving the embezzlement of over US$4.5 billion from Malaysia’s sovereign wealth fund, implicating political leaders, financiers, and global banks. Part II will discuss Goldman Sachs’ role in the 2008 financial crisis and its long list of scandals. We will also talk in detail about Jack Ma in Part II of this series.

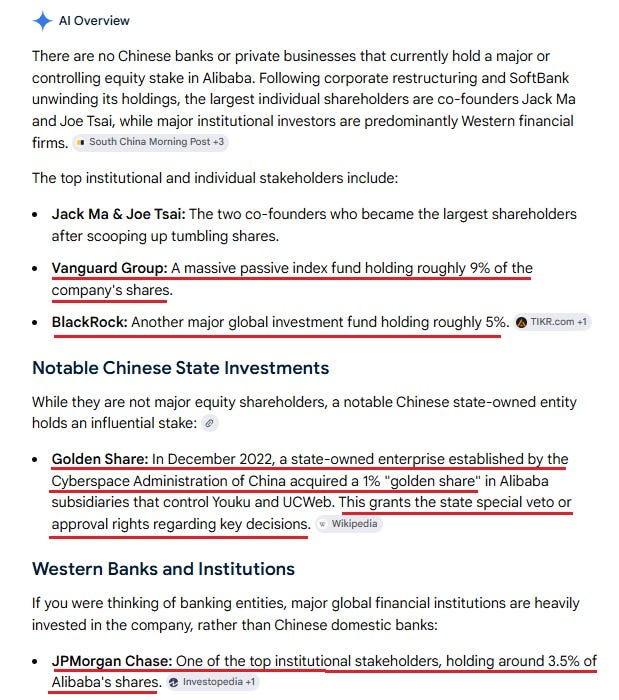

Who are the major shareholders of Alibaba Group?

Interestingly, after Jack Ma and Joseph Tsai the largest shareholders of Alibaba are Vanguard with 9% and BlackRock with 5%. The Vanguard Group, Inc. is an American registered investment adviser with approximately $12 trillion in global assets under management as of 2025. It is the largest provider of mutual funds and the second-largest provider of exchange-traded funds (ETFs) in the world after BlackRock’s iShares.

Then we have JPMorgan Chase with a 3.5% shareholding.

Finally, we have the “Golden Share”, the only Chinese state-owned entity that hold an influential stake of 1%, which is the Cyberspace Administration of China, established in Dec. 2022. I think it is pretty obvious what this really is. After the clamp down on Alibaba and Jack Ma in particular in 2020, moves like this from the Chinese government are part of the reigning in of Big Tech. The “golden share” gives the Chinese government the right to veto or approve any key decisions made in the Alibaba’s Group structure, function and direction.

Perhaps this is the reason why Masayoshi Son from SoftBank dropped Jack Ma like a sack of potatoes? He could see the writing on the wall that the Alibaba Group would not be an easy conduit for Project Stargate into China.

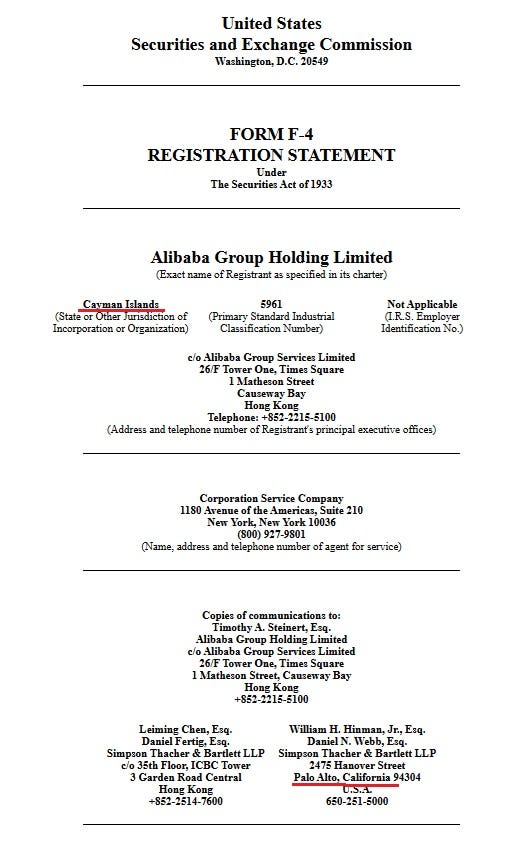

Where is Alibaba Group registered you might ask? In the British Cayman Islands of course!

It should be noted here that not just any company can be accepted as registered in the British Cayman Islands. This is a select elite club for off-shore haven status. The fact that the “Chinese” Alibaba Group is registered in the Cayman Islands shows where its true colors are at.

In addition, note that other locations included in its registration statement are the historically British Hong Kong which still has its own legal system separate from China’s mainland, and New York.

Interestingly of the addresses given for copies of communications are Palo Alto, California. Palo Alto is a Project Stargate hub.

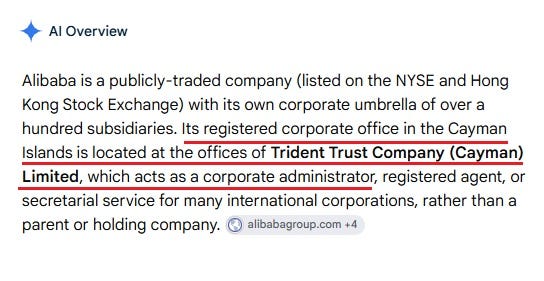

Trident Trust was founded in London in 1978 as a privately owned and independent provider of corporate, fiduciary and fund administration services. In 1983, Trident Trust expanded beyond the UK with an office in Jersey, in the centre of St. Helier, to “serve clients and explore new opportunities in offshore markets.”[104]

The island Jersey is an infamous British off-shore haven, a self-governing British Crown Dependency to be exact.

The following year, 1984, marked the company presence in the U.S. and Caribbean and U.S. Virgin Islands. And then later into the British Virgin Islands. For more on the relevance of offshore havens refer to my paper here.

Now let us move on to what is behind the creation of Tencent. Because the length of this paper is already quite long, I will focus here on strictly who built up Tencent, while in Part II we will discuss the function of Tencent in detail.

Interestingly, the origin story of Alibaba Group and Tencent have a lot of similarities. Pony Ma, along with four other individuals[105] are credited as the founders of Tencent. However, when we look into Tencent deeper we soon find that the true brain of the operation is Martin Lau, the Executive Director and President of Tencent.

Martin Lau born in Beijing was raised in British Hong Kong and was educated in the United States, graduating from University of Michigan, Northwestern University and Stanford (Project Stargate recruitment hub).[106] Lau studied Science and Electrical Engineering at both Michigan and Stanford and gained an MBA from Northwestern.

After graduating, Lau was hired by the incredibly competitive and prestigious management consultant firm McKinsey & Company before joining Goldman Sachs.

Interestingly, we come across another powerful institution caught up in the opioid epidemic which China is typically blamed for: McKinsey & Company.

McKinsey & Company, headquartered in New York City, has been the subject of significant controversy and is the subject of multiple criminal investigations into its business practices. The company has been criticized for its role promoting OxyContin use throughout the opioid crisis in North America.[107] [108]

McKinsey & Co. has also drawn controversy for its involvement with the notorious Purdue Pharma,[109] basically the cause for America’s opioid crisis. For more on Purdue Pharma refer to my paper here.

McKinsey advised opioid makers on how to “turbocharge” sales of OxyContin, proposed strategies to counter the emotional messages from mothers with teenagers who overdosed on OxyContin, and helped opioid makers circumvent regulation.[110]

McKinsey & Co. also advised Purdue Pharma to offer pharmacies rebates based on the number of overdoses and addictions they caused.[111] Records show that McKinsey worked for Purdue Pharma and other opioid makers in a 15-year period, from 2004 to 2019.[112]

In February 2021, McKinsey paid $600 million to settle investigations into its role in promoting sales of OxyContin and fuelling the greater opioid epidemic.[113] In April 2022, the New York Times reported that McKinsey had frequently allowed partners and other consultants to work for both government clients, such as the FDA, and pharmaceutical clients, such as Purdue.[114] These actions violated McKinsey’s own internal ethical guidelines.

In December 2023, Reuters reported that McKinsey had agreed to pay an additional $78 million to settle claims with health insurers McKinsey’s consulting helped to fuel “an epidemic of opioid addiction through its work for drug companies”.[115] Reuters reported the settlement would be the last in a series and that McKinsey “admitted to no wrongdoing.”

‘In 2024, the company became the subject of a criminal investigation by the U.S. Justice Department into its role in advising opioid manufacturers how to boost sales. A grand jury was convened to determine charges to be brought against the firm. It is also under investigation for obstruction of justice during the period that concerns were mounting about their activities. The firm settled the investigation in December 2024, for a sum of $650 million and with conditions that it cannot market controlled substances for a period of five years. This agreement was filed in federal court in Abingdon, Virginia, with aims to resolve criminal charges which were brought up as part of the latest corporate prosecution concerning the marketing of addictive painkillers.’[116]

McKinsey & Co. have also worked with ICE and the Riker Island jail complex with their fair share of controversy.[117]

McKinsey & Co. has been associated with a number of other notable scandals, including the 2008 financial crisis[118] and facilitating state capture in South Africa.[119] We will talk about these role in further detail in Part II of this series.

Back to Martin Lau.

After Martin Lau worked as a management consultant for the notorious McKinsey & Co. he joins Goldman Sachs and becomes the Chief Operating Officer of the Telecommunications, Media and Technology (TMT) group in the Investment Banking Division of Goldman Sachs Asia.[120]

Interestingly, in 2004 Lau meets Pony Ma (founder of Tencent) while working for Goldman Sachs’ handling of Tencent’s IPO. Once again, similar to the story of Joseph Tsai and Jack Ma (no relation to Pony Ma), Lau is so enthusiastic about Tencent, which is still in its humble stage, that he quits his incredibly prestigious job with Goldman Sachs worth tens of millions in salary to work for Tencent.

Lau within a short period becomes the Chief Strategy and Investment Officer of Tencent, responsible for the company’s strategy, investments, mergers and acquisitions, and investor relations.[121] Basically Lau is running the Tencent ship, like Joseph Tsai’s (along with Goldman Sachs J. Michael Evans) running of Alibaba.

Looks increasingly like Goldman Sachs is running the show doesn’t it?

In 2007 Lau is promoted to Executive Director in 2007 and served as a Non-executive Director of Kingsoft in 2011. In 2012, he became the Chairman of Tencent E-commerce Holdings, during which he promoted strategic partnerships such as investments in JD.com (backed by Tencent) [122] and Didi Chuxing. Martin Lau has served on the board of JD.com, Didi Chuxing, Tencent Music, Kingsoft, and Meituan.[123]

Recall, that Bank of America Merrill Lynch and UBS were not part of the Alibaba IPO because they were working on the IPO of Tencents’ JD.com. Interestingly, Goldman Sachs man, Martin Lau served on both the board of JD.com and Tencent. Small world…if you work for Goldman Sachs that is.

Martin Lau’s Baidu Wiki page writes:[124]

Before Lau joined, Tencent rarely used external investment methods, preferring to invest internally in departments like R&D, pursuing whatever was trending. This [Martin Lau’s] approach led to Tencent’s rapid development in areas such as gaming, portals, and internet value-added services, ushering in the company’s subsequent “golden five years.”

Who owns Tencent’s holdings?

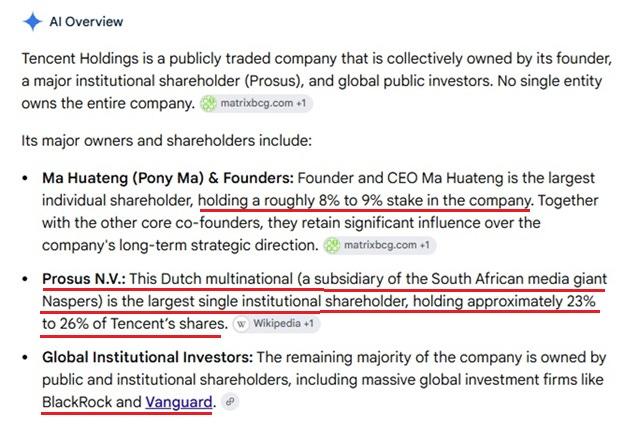

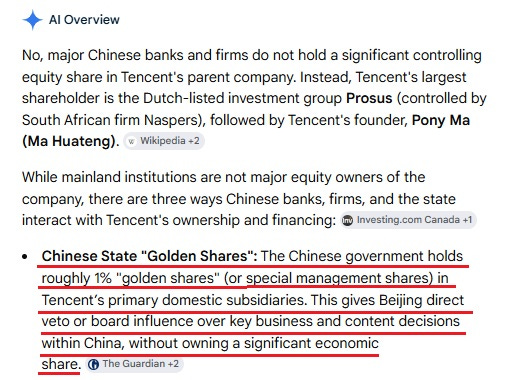

Prosus Naspers is the majority stakeholder of Tencent, some estimates go as high as a 29% stake, is headquartered in South Africa, historically part of the British Empire. Prosus and Naspers are technically two different entities that hold majority stake in each other. Naspers has a particularly notorious history, and was heavily involved in the South African apartheid, more on this later in this series.

Suffice to say for now, that is an interesting majority stakeholder for Tencent to have, is it not? Note that BlackRock and Vanguard are again, like the case of Alibaba, among the most significant stakeholders of Tencent.

Another thing that should be noted here is that there are no Chinese state-owned institutions, banks or businesses that hold significant stake in either Alibaba or Tencent. Hmmmm…..

As in the case with Alibaba, Tencent has also given the Chinese government a 1% “golden share” which is a fancy way of saying that the Chinese government has the right to veto or approve of any major decisions that Tencent makes in its current and future structuring.

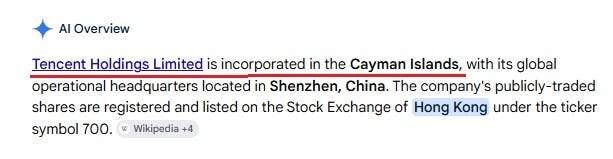

And where is Tencent registered? You guessed it, the Cayman Islands yet again!

Goldman Sachs as the Common Denominator

I imagine the prevalence of Goldman Sachs role in not only Alibaba and Tencent has been clearly pronounced for you at this point, but as we will see in Part II of this series, Goldman Sachs also played a central role in the 2008 financial crisis.

For now, let us look further into where the Goldman Sachs tentacles have reached. This will be done here summarily since this paper is getting quite long, however, this discussion will be continued in further detail throughout this series.

First let us look into Goldman Sachs relationship with Project Stargate.

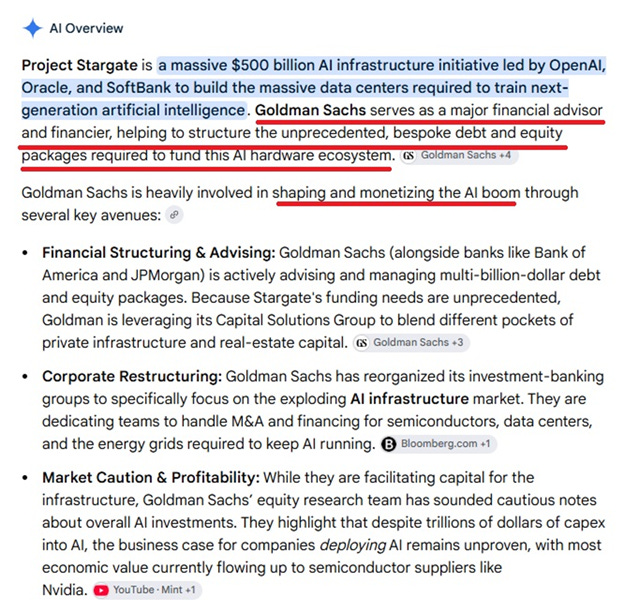

Thus, Goldman Sachs is the major financial advisor and financier of Project Stargate and is a leader in shaping and monetizing the AI boom.

Let us look at Goldman Sachs relationship to SoftBank.